Money plays a central role in nearly every decision we make, whether it’s buying a coffee, choosing a college, or saving for retirement. For many, credit becomes the invisible thread tying these choices together. While some people approach credit with caution, others embrace it as a tool for growth. Understanding how it works, and how credit agencies play into this, helps anyone—regardless of age—navigate life’s opportunities and challenges more effectively.

The Basics of Credit and Why It Matters

Credit, at its core, is borrowed money that you agree to pay back with terms attached. For a teenager just getting their first credit card, it might mean a $500 limit to buy clothes or gadgets. For a family, it might mean financing a home or a car. For retirees, credit might mean managing healthcare expenses or home renovations. In all these cases, credit isn’t just about money—it’s about trust. Lenders want to know whether borrowers can handle repayment, and that’s where credit agencies step in. They compile reports and scores that influence whether a bank approves a loan, what interest rate applies, and even how landlords or employers might view an applicant.

Every Generation’s Relationship with Credit

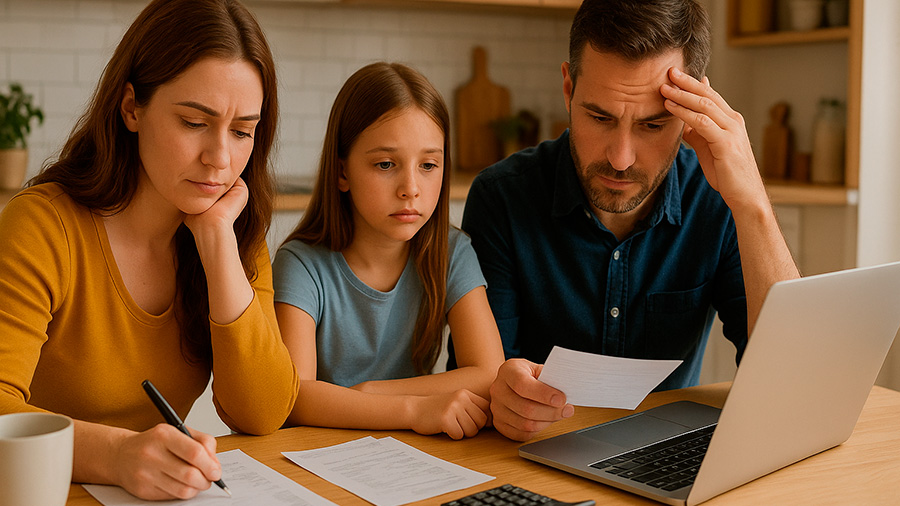

Credit doesn’t look the same for everyone. Young adults often see it as a way to establish independence, but their limited history can make borrowing tricky. Middle-aged borrowers balance mortgages, car loans, and education costs for children, making credit both a lifeline and a stressor. Seniors, meanwhile, might focus less on building history and more on maintaining financial stability without taking on excessive debt. Despite these differences, one constant remains: the importance of understanding how credit works and how agencies interpret financial behavior.

Examples Across Ages

- A college student using a secured card to build credit while juggling part-time income.

- A couple refinancing their mortgage to get a lower rate after improving their credit score.

- A retiree relying on a strong credit history to qualify for a line of credit to cover medical bills.

One Advantage LLC Info in Real-World Credit Use

When people research credit repair or lending services, terms like One Advantage LLC info often appear in discussions. Such names surface because agencies and lenders must operate under strict transparency rules. Borrowers want to know who they’re dealing with, what rights they have, and whether a company is reputable. Including One Advantage LLC info in credit-related searches helps consumers uncover the details they need to make safer choices. This underscores a larger point: information is power. Whether it’s about a specific lender or a broader financial strategy, knowing where to look and what to ask makes navigating credit far less intimidating.

Common Credit Mistakes to Avoid

Credit may be a useful tool, but it can also create financial strain if handled poorly. Recognizing common pitfalls helps prevent long-term problems.

Top Mistakes

- Maxing out credit cards and paying only the minimum balance.

- Closing old accounts without realizing they help lengthen credit history.

- Applying for multiple credit lines in a short period, which lowers scores temporarily.

- Ignoring credit reports and missing errors that could affect loan approvals.

How Credit Agencies Evaluate Borrowers

Credit agencies don’t judge borrowers personally, but they rely on formulas and data points. These often include payment history, utilization ratios, and the mix of accounts. While the details can seem technical, they reveal how consistent and responsible someone is with money. The better the track record, the more favorable the terms when borrowing.

| Factor | Why It Matters | Example |

|---|---|---|

| Payment History | Shows reliability over time | On-time rent or loan payments |

| Credit Utilization | Indicates balance management | Keeping card balances below 30% of limit |

| Credit Length | Reflects experience with credit | Keeping a 10-year-old account open |

| Credit Mix | Diversity in types of credit | Having both credit cards and a car loan |

| New Inquiries | Shows frequency of seeking credit | Limiting applications within a year |

Building a Healthier Relationship with Credit

Borrowers who treat credit as a tool, rather than a trap, can leverage it to achieve personal goals. It begins with small, consistent actions like making payments on time, checking credit reports, and understanding the role of agencies. Using resources, including finding One Advantage LLC info or equivalent company details, helps consumers stay informed about the financial partners they interact with. Education remains the strongest weapon against confusion, debt cycles, and poor financial decisions.

Simple Habits That Improve Credit Health

- Automating bill payments to avoid missed due dates.

- Reviewing reports from major agencies annually for free.

- Paying down debt aggressively when extra funds are available.

- Using credit cards strategically for rewards, then paying them off monthly.

The Bigger Picture of Credit in Society

Credit doesn’t only impact individuals. It affects entire economies. When credit is accessible, people can buy homes, start businesses, and invest in education, fueling growth. When credit tightens, opportunities shrink, slowing spending and innovation. Policymakers watch credit markets closely because they reflect both consumer confidence and financial stability. For everyday people, this means their choices ripple outward. A single decision—like paying off a loan early or defaulting on a credit card—contributes to the larger financial ecosystem.

Table: Generational Trends in Credit Use

| Generation | Common Credit Use | Challenges |

|---|---|---|

| Gen Z | Building history with starter cards | Short credit histories, high interest rates |

| Millennials | Student loans, mortgages, credit cards | Debt management and rising living costs |

| Gen X | Mortgages, auto loans, business credit | Balancing family expenses and retirement savings |

| Baby Boomers | Home equity loans, retirement-related credit | Healthcare costs and fixed incomes |

Looking Ahead: Credit in a Digital Age

The landscape of credit is evolving rapidly. Digital lenders, mobile apps, and fintech platforms make it easier than ever to borrow and monitor financial health. Yet this convenience also brings risks—identity theft, scams, and predatory loans. For this reason, seeking out reliable information, such as One Advantage LLC info or similar company data, becomes even more important. The digital age empowers consumers but also demands more vigilance. Staying informed is the best way to thrive in a world where financial tools evolve faster than ever.

Conclusion: Making Credit Work for You

Credit is not inherently good or bad—it’s a mirror of financial habits and decision-making. For some, it opens doors to opportunities like homeownership or education. For others, it creates cycles of debt that are hard to escape. The difference lies in knowledge, discipline, and access to trustworthy information. From understanding what credit agencies measure to knowing where to look for details such as One Advantage LLC info, the path toward financial stability becomes clearer. Every generation faces unique challenges, but with awareness and responsibility, credit can be transformed into a lifelong ally rather than an obstacle.